THE IDEOLOGY OF THE 99%

THE IDEOLOGY OF THE 99%

Why did #OccupyWallStreet strike such a chord?

Hey Folks,

Today I’m continuing with the Occupy Wall Street theme.

If you’re wondering where I’m going with this, I’ll tell you. I think that a populist resistance movement which focuses on opposing the banks is the way to build unity in a deeply polarized America.

Leftists need to realize that many right-wing people hate the banks just as much as they do, if not more.

This is a significant point of unity that can serve as a basis for a populist movement. But talking about ending capitalism is a non-starter for most Americans, because they’ve believed that capitalism is the opposite of communism their whole lives. And if you look at things from their perspective, you’ll see they’re not necessarily wrong. They’re just using words differently.

To them, capitalism simply means free enterprise. I’m certainly not opposed to free enterprise. Are you?

What I’m opposed to is the rich monopolizing the resources others need to survive in order to force them to accept socioeconomic conditions that no one in their right mind would voluntarily consent to.

I’m also opposed to usury, which gives me an important point of unity with religious people. If you didn’t know, both Christianity and Islam explicitly forbid usury, though many have gotten squishy on that point in modern times.

Also, there are many conservatives who agree wholeheartedly that fractional reserve banking is a scam and that the Federal Reserve is massive scam. They’re right.

If we can put aside issues that the ruling class loves to use to divide us, it may be possible to build a populist movement able to fight back against the criminocracy rapidly transforming our world into a dystopian nightmareland.

I won’t shut up about David Graeber because I believe that his ideas are our best hope for figuring out how to build that populist movement.

I will quickly mention that the selection you are about to read includes him talking some smack about the Tea Party, the right-wing populist movement which arose in the aftermath of the 2008 bank bailouts. According to Graeber, the Tea Party was opposed to those bailouts for the wrong reasons. This is a great example of sectarianism that we need to overcome. Occupy Wall Street and the Tea Party were opposed to the same thing. They should have joined forces.

The fact of the matter is that the U.S. Left is dead as a doorknob, and there’s no practical alternative for Leftists who wish to organize politically than to reassess their prejudices and expand their minds.

If you actually take the time to talk to blue-collar, working class people, you might find that they care about many of the same things that you do.

The time has come to put aside our differences. The hour is late.

Love & Solidarity,

Crow Qu’appelle

Why did Occupy spread so quickly across America?

By David Graeber, excerpted from The Democracy Project.

When she wasn’t helping with logistics and organizing facilitation trainings, Marisa Holmes spent much of her time during the early days of the occupation video-recording one-on-one interviews with fellow campers. Over and over, she heard the same story: “I did everything I was supposed to! I worked hard, studied hard, got into college. Now I’m unemployed, with no prospects, and $20,000 to $50,000 in debt”.

Some of these campers were from solidly middle-class families. More seemed children of relatively modest backgrounds who had worked their way into college by talent and determination, but whose lives were now in hock to the very financial industries that had trashed the world economy and found themselves entering a job market almost entirely bereft of jobs. Stories like this struck a chord with me, since I had been spending much of that summer giving lectures on the history of debt. I tried to keep my life as an author apart from my life as an activist, but I found it increasingly difficult, since every time I’d give a talk with an appreciable number of young people in attendance, at least one or two would approach me afterward to ask about the prospects of creating a movement over the issue of student loans. One of the themes of my work on debt was that its power lies in intense moral feelings it invokes, against the lenders and, more to the point, against the indebted themselves: the feelings of shame, disgrace, and violent indignation from being told, effectively, that one is the loser in a game no one forced one to play. Of course anyone who does not wish to spend the rest of their life as a dishwasher or sales clerk —in other words, in a job with no sorts of benefits, knowing one’s life could be destroyed by a single unforeseen illness— has been led to believe that they have no choice but to pursue higher education in America, which means one effectively begins one’s life as a debtor. And to begin one’s life as a debtor is to be treated as if one already lost.

Some of the stories I heard during my tour were extraordinary. I particularly remember a grave young woman who approached me after a reading at a radical bookstore to tell me that though of modest origins, she had managed to work her way into a Ph.D. in Renaissance literature at an Ivy League college. The result? She was $80,000 in debt, with no immediate prospects of anything but adjunct work, which couldn’t possibly cover her rent, let alone her monthly loan payments. “So you know what I ended up doing?” she asked me. “I’m an escort! It’s pretty much the only way to get enough cash to be able to have any hope of getting out of this. And don’t get me wrong, I don’t regret the years I spent in graduate school for a moment, but you have to admit it’s a little bit ironic”.

“Yes”, I said, “not to mention a remarkable waste of human resources”.

Perhaps the image stuck to me because of my personal history —I often think I represent the last generation of working-class Americans who had any sort of realistic shot at joining the academic elite through sheer hard work and intellectual attainment (and even in my case it turns out to have been temporary). Partly because the woman’s story brought home the degree to which debt is not only hardship, but degradation. After all, we all know what sort of people frequent expensive escorts in New York City. There was, right after 2008, a moment where it looked like Wall Street spending on cocaine and sexual services was going to have to be retrenched somewhat; but after the bailouts, like spending on expensive cars and jewelry, it appears to have rapidly shot up again. This woman was basically reduced to a situation where the only way she could pay her loans was to work fulfilling the sexual fantasies of the very people who had loaned her the money, and whose banks her family’s tax dollars had just bailed out. What’s more, her case was just an unusually dramatic example of a nationwide trend. For debt-strapped women in college (and remember, a growing majority of those seeking higher education in America today are women), selling one’s body has become a growing —last, desperate— expedient to those who see no other way to finish their degree. The manager of one website that specializes in matching sugar daddies with those seeking help with student loans or school fees estimates he already has 280,000 college students registered. And very few of these are aspiring professors. Most aspire to little more than a modest career in health, education, or social services.

It was stories like that I had in the back of my mind when I wrote a piece for The Guardian about why the Occupy movement had spread so quickly. The piece was meant to be part descriptive, part predictive:

We are watching the beginnings of the defiant self-assertion of a new generation of Americans, a generation who are looking forward to finishing their education with no jobs, no future, but still saddled with enormous and unforgiveable debt. Most, I found, were of working class or otherwise modest backgrounds, kids who did exactly what they were told they should, studied, got into college, and are now not just being punished for it, but humiliated —faced with a life of being treated as deadbeats, moral reprobates. Is it really surprising they would like to have a word with the financial magnates who stole their future?

Just as in Europe, we are seeing the results of colossal social failure. The occupiers are the very sort of people, brimming with ideas, whose energies a healthy society would be marshalling to improve life for everyone. Instead they are using it to envision ways to bring the whole system down.

The movement has diversified far beyond students and recent graduates, but I think for many in the movement the concern with debt and a stolen future remains a core motivation for their involvement. It’s telling to contrast the Occupy movement in this way with the Tea Party, with which it is so often compared. Demographically, the Tea Party is at its core a movement of the middle-aged and well-established. According to one poll in 2010, 78 percent of the Tea Partiers were over the age of thirty-five, and about half of those, over fifty-five. This helps explain why Tea Partiers and occupiers generally take a diametrically opposite view of debt. True, both groups objected in principle to government bailouts of the big banks, but in the case of the Tea Partiers, this is largely rhetoric. The Tea Party’s real origins go back to a viral video of CNBC reporter Rick Santelli speaking from the floor of the Chicago Mercantile Exchange on February 19, 2009, decrying rumors that the government might soon provide assistance to indebted homeowners: “Do we really want to subsidize the losers’ mortgages?” Santelli asked, adding, “This is America! How many of you people want to pay for your neighbor’s mortgage that has an extra bathroom and can’t pay their bills?” In other words, the Tea Party originated as a group of people who at least imagined themselves as creditors.

Occupy, in contrast, was and remains at its core a forward-looking youth movement —a group of forward-looking people who have been stopped dead in their tracks. They played according to the rules and watched the financial class completely fail to play by the rules, destroy the world economy through fraudulent speculation, get rescued by prompt and massive government intervention, and, as a result, wield even greater power and be treated with even greater honor than before, while they are relegated to a life of apparently permanent humiliation. As a result, they were willing to embrace positions more radical than anything seen, on a mass scale, in America for generations: an explicit appeal to class politics, a complete reconstruction of the existing political system, a call (for many at least) not just to reform capitalism but to begin dismantling it entirely.

That a revolutionary movement emerged from such a situation is hardly new. For centuries now, revolutionary coalitions have always tended to consist of a kind of alliance between children of the professional classes who reject their parents’ values, and talented children of the popular classes who managed to win themselves a bourgeois education, only to discover that acquiring a bourgeois education does not actually mean one gets to become a member of the bourgeoisie. You see the pattern repeated over and over, in country after country: Chou En-lai meets Mao Zedong, or Che Guevara meets Fidel Castro. U.S. counterinsurgency experts have long known the surest harbinger of revolutionary ferment in any country is the growth of a population of unemployed and impoverished college graduates: that is, young people bursting with energy, with plenty of time on their hands, every reason to be angry, and access to the entire history of radical thought. In the United States, you can add to these volatile elements the depredations of the student loan system, which ensures such budding revolutionaries cannot fail to identify banks as their primary enemy, or to understand the role of the federal government —which maintains the student loan program, and ensures that their loans will be held over their heads forever, even in the event of bankruptcy— in maintaining the banking system’s ultimate control over every aspect of their future lives. As n+1’s Malcolm Harris, who writes frequently on generational politics in America, puts it:

Today, student debt is an exceptionally punishing kind to have. Not only is it inescapable through bankruptcy, but student loans have no expiration date and collectors can garnish wages, social security payments, and even unemployment benefits. When a borrower defaults and the guaranty agency collects from the federal government, the agency gets a cut of whatever it’s able to recover from then on (even though they have already been compensated for the losses), giving agencies a financial incentive to dog former students to the grave.

It’s also not surprising that, when the Great Recession that we’re still struggling through struck in 2008, young people were its most dramatic victims. In fact, this generation’s prospects were, in historical terms, uniquely bleak even before the economy collapsed. The generation of Americans born in the late 1970s is the first in U.S. history to face the prospect of living standards lower than their parents’. By 2006, this generation was worse off than their parents at a similar age in almost every register: they received lower wages and less benefits, were more indebted, and are far more likely to be either unemployed or in jail. Those who entered the workforce on finishing high school could expect to find themselves lower-paying jobs than their parents found, and ones that are far less likely to provide benefits (in 1989, almost 63.4 percent of high school graduates got jobs that provided health care; now, twenty years later, the number is 33.7 percent). Those that entered the workforce after finishing college or university found themselves with better jobs, back when there were jobs, but since the cost of higher education has been growing at a rate that outstrips any other commodity in U.S. history, larger and larger portions of this generation have been graduating with crippling levels of debt. In 1993, less than half of those who left college, left indebted. Now the proportion is over two thirds; basically, all but the very most financially elite.

The immediate effect of this was to destroy much of what was most valuable in the college experience itself, which had once been the only four years of genuine freedom in an American’s life: a time to not only pursue truth, beauty, and understanding as values in themselves, but to experiment with different possibilities of life and existence. Now all of this was relentlessly subordinated to the logic of the market. Where once universities held themselves out as embodiments of the ancient ideal that the true purpose of wealth is to afford one the means and leisure to pursue knowledge and understanding of the world, now the only justification for knowledge was held to be to facilitate the pursuit of wealth. Those who insisted on treating college as anything but a calculated investment —those who, like my friend at the radical bookstore, had the temerity to wish to contribute to our understanding of the sensibilities of English Renaissance poetry despite an uncertain job market— were likely to do so at a terrible personal cost.

So the initial explanation for the spread of the movement is straightforward enough: a population of young people with a good deal of time, and every reason to be angry —and among whom the most creative, idealistic, and energetic tended to have reason to be angriest of all. Yet this was just the initial core. To become a movement it had to appeal to a much larger section of the population. And again, very quickly, this began to happen.

Here, too, we witnessed something extraordinary. Beyond students, the constituencies that rallied the most quickly were, above all, working class. This might not seem that surprising considering the movement’s own emphasis on economic inequality; but in fact it is. Historically, those who have successfully appealed to class populism in the United States have done so largely from the right, and have focused on professors more than plutocrats. In the weeks just before the occupation, the blogosphere had been full of contemptuous dismissals of appeals for educational debt relief as the whining of pampered elitists. And it’s certainly true that historically the plight of the indebted college graduate would hardly be the sort of issue that would speak directly to the hearts of, say, members of New York City’s Transit Workers Union. But this time it clearly did. Not only were the TWU’s leaders some of the earliest and most enthusiastic endorsers of the occupation, with avid support from rank and file, they actually ended up suing the New York Police Department for commandeering their buses to conduct the mass arrest of OWS activists blocking the Brooklyn Bridge. This leads to [another] question:

Why would a protest by educated but indebted youth strike such a chord across working-class America —in a way that it almost certainly would not have in 1967, or even 1990?

Some of it, perhaps, lies in the fact that the lines between students and workers have somewhat blurred. Most students turn to paid employment at least at some point in their college careers. Furthermore, while the number of Americans entering college has grown considerably over the last twenty years, the number of graduates remains about the same; as a result, the ranks of the working poor are now increasingly filled with dropouts who couldn’t afford to finish their degrees, still paying for those years they did attend, usually still dreaming of someday returning. Or who still carry on as best they can, juggling part-time jobs and part-time classes.

When I wrote the story in The Guardian, the discussion section was full of the usual dismissive comments: these were a bunch of pampered children living off someone else’s dime. One commentator was obsessed by the fact that several of the women protesters immortalized in press photos had pink hair. This was held out as proof that they existed in a bubble of privilege, apart from “real” Americans. One thing clear about such commentators was that they had never spent very much time in New York. Just as styles that were in the 1960s identified with hippies —long hair, hash pipes, ripped T-shirts— became, by the 1980s, a kind of uniform for casually employed working-class youth in much of small-town America, so has much of the style of the 1980s punk movement, pink hair, tattoos, piercings —come to play the same role today for the precarious, unsteadily employed, working class in America’s great metropolises. One need only look around at the people preparing one’s coffee, delivering one’s packages, or moving one’s furniture.

One reason the old 1960s antipathy between “hippies and hard hats” has dissolved into an uneasy alliance, then, is partly because cultural barriers have been overcome, and partly because of the changing composition of the working class itself, the younger elements of which are far more likely to be entangled in an increasingly exploitive and dysfunctional higher education system. But there is another, I suspect, even more critical element. This is the changing nature of capitalism itself.

There has been much talk in recent years about the financialization of capitalism, or even in some versions the “financialization of everyday life”. In the United States and much of Europe, this has been accompanied by deindustrialization; the U.S. economy is no longer driven by exports, but by the consumption of products largely manufactured overseas, paid for by various forms of financial manipulation. This is usually spoken of in terms of the dominance of what’s called the FIRE sector (Finance, Insurance, Real Estate) in the economy. For instance, the share of total U.S. corporate profits derived from finance alone has tripled since the 1960s:

Even this breakdown underestimates the numbers considerably, since it only counts nominally financial firms. In recent decades almost all manufacturers have gone into the finance business, and this accounts for much of their profits as well. The reason the auto industry collapsed during the financial meltdown of 2008, for example, was that companies like Ford and GM had by then for years been earning almost all of their profits not from making cars, but from financing them. Even GE earned about half its profits from its financial division. So while by 2005, 38 percent of total corporate profits derived from finance companies, the real number was probably more like half when you count the finance-related profits of companies whose ostensible business was nonfinancial. Meanwhile, only about 7 or 8 percent of all profits came from industry.

When in 1953, GM chairman Charles Erwin Wilson coined the famous phrase “What’s good for General Motors is good for America”, it was taken in many quarters as the ultimate statement of corporate arrogance. In retrospect, it has become easier to see what he really meant. At that time, the auto industry generated enormous profits; the lion’s share of the money that flowed into companies like GM and their executives was delivered directly to government coffers as taxes (the regular corporate tax rate under President Dwight Eisenhower was 52 percent, and the top personal tax rate, that applied for instance to corporate executives, 91 percent). At the time, the bulk of government revenue was derived from corporate taxes. High corporate taxes encouraged executives to pay higher wages (why not distribute the profits to one’s workers, and at least gain the competitive advantage of grateful and loyal employees, if the government would otherwise take it anyway?); government used the tax revenue to build bridges, tunnels, and highways. These construction projects, in turn, not only benefited the auto industry, they created even more jobs, and gave government contractors the opportunity to enrich the politicians who distributed the booty with hefty bribes and kickbacks. The results might have been ecologically catastrophic, especially in the long term, but at the time, the relationship between corporate success, taxes, and wages seemed like a surefire engine for permanent prosperity and growth.

Half a century later we are clearly living in a different economic universe. The profits to be won from industry have shriveled. Wages and benefits have stagnated or declined; infrastructure is crumbling. However, in the 1980s when Congress eliminated the usury laws (opening the way to a world where U.S. courts and police served as enforcers to loans that can go as high as 300 percent annual interest, the sort of arrangements one could previously only make with organized crime), they also allowed almost any corporation to go into the finance business. The word “allowed” in the last sentence may strike you as strange, but it’s important to understand that the language we typically use to describe this period is profoundly deceptive. For instance, we usually speak of changes in legislation surrounding finance as a matter of “deregulation”, of the government stepping out of the way and letting corporations play the market however they like. Nothing can be further than the truth. By allowing any corporation to become part of the financial services industry, government was granting them the right to create money. This is because banks, and other lenders, do not, generally speaking, lend money they already have. They create the money by making loans. (This is the phenomenon Henry Ford was referring to when he made his famous comment that if the American people were ever to figure out how banking really works, “there would be a revolution before tomorrow morning”. The Federal Reserve creates money and loans it to banks that are allowed to lend ten dollars for every one they hold as reserves; thus, effectively, allowing them to create money). True, the financial divisions of car companies were limited to creating money that would be returned to them to buy their own cars, but the arrangement allowed them to derive hefty profits from interest, fees, and penalties, and eventually those finance-related profits dwarfed profits from the cars themselves. At the same time, corporations like GM, GE, and the rest were, like the largest banks, in many cases paying no federal taxes at all. Insofar as their profits went to the government, it was given directly to politicians in the form of bribes —bribery having been renamed “corporate lobbying”— to convince them to enact further legislation, often written by the companies themselves, facilitating further extractions from citizens caught in their web of credit. And since the IRS was no longer receiving any appreciable amount of revenue from corporate taxes, the government, too, was increasingly in the business of extracting its money directly from citizens’ personal incomes, or, in the case of now cash-strapped local governments, from a remarkably similar campaign of multiplying fees and penalties.

If the relation between corporations and government in the 1950s bears little resemblance to the mythical “free market capitalism” on which America is supposed to be founded, in the case of current arrangements it’s hard to see why we are still using the word “capitalism” at all.

Back when I was in college, I learned that capitalism was a system where private firms earned profits by hiring others to produce and sell things; on the other hand, systems in which the big players simply extracted other people’s wealth directly, by threat of force, were referred to as “feudalism”. By this definition, what we call “Wall Street” has come to look, increasingly, like a mere clearinghouse for the trading and disposal of feudal rents, or, to put it more crudely, scams and extortion, while genuine 1950s-style industrial capitalists are increasingly limited to places like India, Brazil, or Communist China. The United States does, of course, continue to have a manufacturing base, especially in armaments, medical technology, and farm equipment. Yet except for military production, these play an increasingly minor role in the generation of corporate profits.

With the crisis of 2008, the government made clear that not only was it willing to grant “too big to fail” institutions the right to print money, but to itself create almost infinite amounts of money to bail them out if they managed to get themselves into trouble by making corrupt or idiotic loans. This allowed institutions like Bank of America to distribute that newfound cash to the very politicians who voted to bail them out and, thus, secure the right to have their lobbyists write the very legislation that was supposed to “regulate them”. This, despite having just nearly destroyed the world economy. It’s not entirely clear why such firms should not, at this point, be considered part of the federal government, other than that they keep their profits for themselves.

Huge proportions of ordinary people’s incomes end up going to feed this predatory system through hidden fees and, especially, penalties. I remember I once allowed a Macy’s clerk to talk me into acquiring a Macy’s charge card, in order to buy a 120 pair of Ray-Ban sunglasses. I sent in a check to pay the charge before leaving the country for an extended trip, but apparently miscalculated by some 2.75 when figuring the tax; when I returned a few months later, I discovered I had accrued something like 500 in late fees. We’re not in the habit of calculating such numbers because they are, even more than debts, seen as the wages of sin: you only pay them because you did something wrong (in my case, miscalculate a math sum and neglect to have the bills forwarded to my overseas address). In fact, the entire system is now geared toward ensuring we make such mistakes, since the entire system of corporate profits depends on them.

How much of the average American’s life income ends up getting passed to the financial services industry in the form of interest payments, fines, fees, service charges, insurance overhead, real estate finder’s fees, and so on? No doubt a defender of the industry would insist some of these are payment for legitimate services —e.g., real estate finder’s fees— but in many cases, these finder’s fees are imposed even on renters who have found apartments themselves. The real estate sector has imposed laws making it effectively impossible to acquire an apartment without paying such a fee. If nothing else, it is clear that there has been a massive increase in such fees in recent decades without any notable increase or improvement in the services provided.

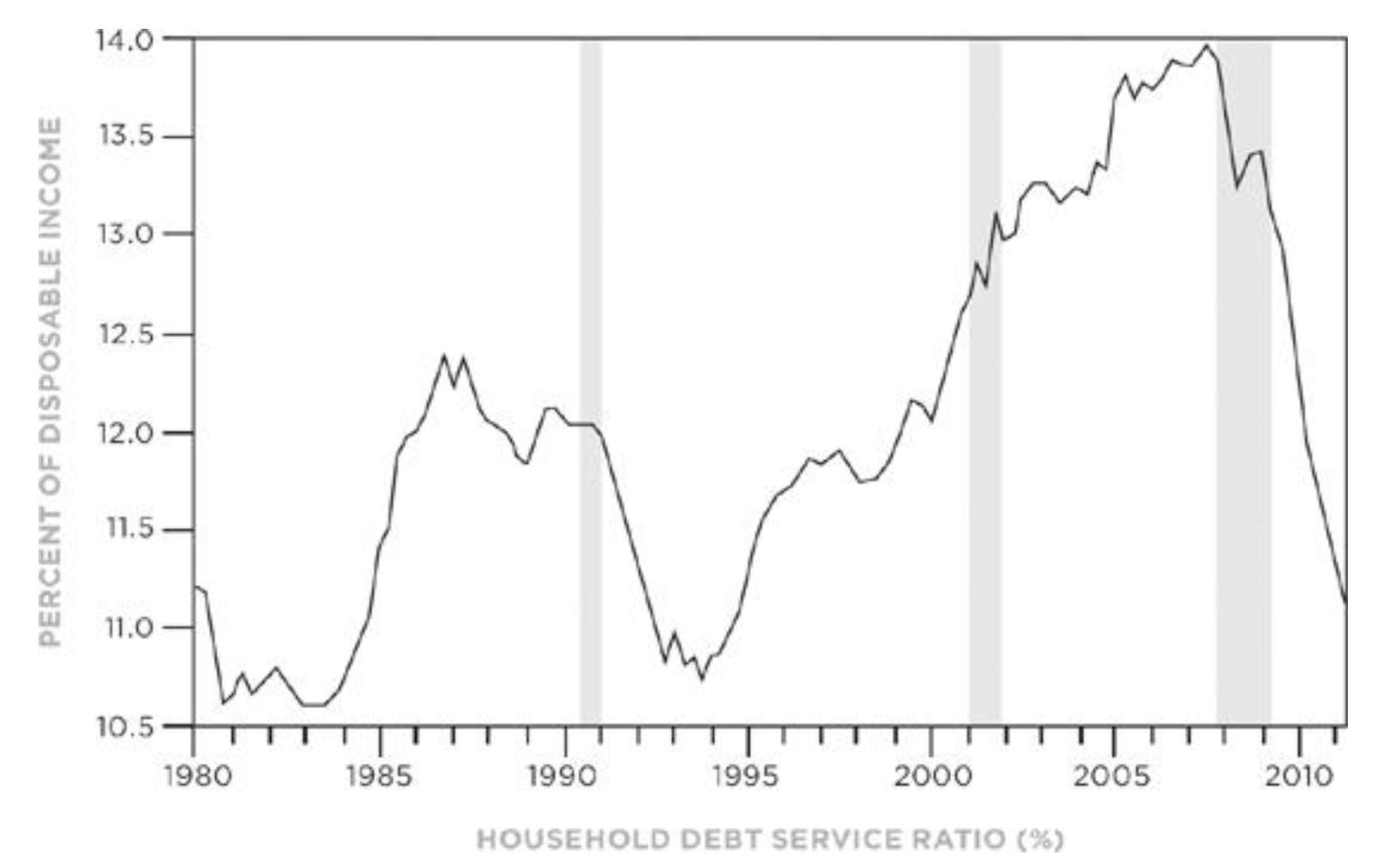

How much of a proportion of the average American family’s income ends up funneled off to the financial services industry? Figures are simply not available. (This in itself tells you something, since figures are available on just about everything else). Still, one can get a sense. The Federal Reserve’s “financial obligations ratio” reports that the average American household shelled out roughly 18 percent of its income on servicing loans and similar obligations over the course of the last decade —it’s an inadequate figure in many ways (it includes principal payments and real estate taxes, but excludes penalties and fees) but it gives something like a ballpark sense.

This already suggests most Americans are delivering as much as one dollar out of five they make directly to Wall Street in one form or another —that is, if you take “Wall Street” in its popular sense, as a code word for the financial sector as a whole. But of course “average Americans” don’t really exist. The depredations of the financial industry fall very unevenly. First of all, while much of this money is simply pocketed by executives at financial companies (all those bankers’ bonuses and so on), some gets redistributed in the form of dividends. Not to everyone, however. Before the crash there was a perception that everyone was in on the deal; that capitalism was becoming a popular enterprise where all Americans, through their investments and retirement accounts, got to own a piece of the action. This was always wildly overstated, and after the crash, when 401(k)s took an enormous hit, but large investors recovered quickly, you don’t hear much of that anymore. No one can really deny that the profit system is still what it always was: a way of redistributing money to those already on the top of the chain. Wealthy Americans, even if they are not employed in the financial sector themselves, end up net winners. Pretty much everyone else has a certain proportion of their income siphoned off.

Those on the bottom of the financial food chain, on the other hand —and this is true any way you measure it, by race, gender, age, employment— invariably end up paying disproportionately more. In 2004, for example, those eighteen to twenty-four ended up paying 22 percent of their income on debt payments (this includes principal, but doesn’t include service charges, fees, and penalties) —with about a fifth paying more than 40 percent— and for twenty-five to thirty-four-year-olds, the cohort most impacted by student loans, things were even worse: they spent an average of a quarter of their income on debts. And these figures are true of younger Americans as a whole, regardless of education. We need hardly speak of the fate of that roughly 22 percent of American households so poor they have no access to conventional credit at all, who have to resort to pawn shops, auto title, or payday loan offices that charge as much as 800 percent annual interest.

And all this was true before the crash!

In the immediate wake of 2008 everyone in America who had any means to reduce their debt, and hence, the amount of their income siphoned off to Wall Street, immediately began to do so —whether by frenetically paying off credit card debt, or walking away from underwater mortgages. This might give a sense of how dramatic was the change:

Yet at the same time, certain types of loans had been set up in such a way that this really wasn’t possible. For example, while it’s possible, if not easy, to renegotiate a mortgage, student loans cannot be; in fact, if you so much as miss a few payments, you are likely to have thousands of dollars in penalties slapped onto the principal. As a result student loan debt continues to balloon at a giddy rate, the total amount owed having long since overtaken total credit card debt and other forms of debt as well:

TOTAL DEBT BALANCE AND ITS COMPOSITION

Aside from students, the other group stuck in the debt trap is the working poor —above all working women and people of color— who continue to see huge chunks of their already stagnating earnings culled directly by the financial services industry. They are often called the “subprimers”, since they are those most likely to have signed up for (or been tricked into) subprime mortgages. Having fallen victim to subprime mortgages with exploding adjustable rates, they are now faced with being harassed by collectors, having their cars repossessed, and, most pernicious of all, having to resort to payday loans for emergency expenses, such as those related to health care, since these are the Americans least likely to have meaningful health benefits. Those paydays operate with annual interest rates of roughly 300 percent a year.

Americans in either of those overlapping categories —the working class and underemployed graduates with crippling student loans— are actually paying more of their income to Wall Street than they pay to the government in taxes.

Back in September, even before the occupation began, Chris —the Food Not Bombs activist who helped us create the first democratic circle in Bowling Green in August— set up a web page on tumblr called “We Are the 99 Percent”, where supporters could post pictures of themselves, holding up a brief account of their life situations. At the time of this writing there are more than 125 pages of these, their authors varying enormously in race, age, gender, and just about everything else.

Recently there was an Internet discussion about the “ideology of the 99 percent” as revealed by these testimonies. It all began when Mike Konczal, of the blog Rortybomb, carried out a statistical analysis to determine the twenty-five most frequently used words in the html texts, and discovered that the most frequent was “job”, the second, “debt”, but that almost all the rest referred to necessities of life, homes, food, health care, education, children (after “job” and “debt”, the next most popular words were: work, college, pay, student, loan, afford, school, and insurance). Glaringly absent was any reference to consumer goods. In trying to understand the implications, Konczal appealed to my own book on debt:

Anthropologist David Graeber cites historian Moses Finley, who identified “the perennial revolutionary programme of antiquity, cancel debts and redistribute the land, the slogan of a peasantry, not of a working class”. And think through these cases. The overwhelming majority of these statements are actionable demands in the form of (i) free us from the bondage of these debts and (ii) give us a bare minimum to survive on in order to lead decent lives (or, in pre-Industrial terms, give us some land). In Finley’s terms, these are the demands of a peasantry, not a working class.

Konczal saw this as a profound diminution of horizons: no longer are we hearing demands for workplace democracy, or dignity in labor, or even economic justice. Under this newly feudalized form of capitalism, the downtrodden are reduced to the situation of medieval peasants, asking for nothing more than the means to make their own lives. But as others soon pointed out, there was a certain paradox here, because ultimately the effect is not to diminish horizons, but to broaden them. Defenders of capitalism have always made the argument that while as an economic system it surely creates vast inequalities, its overall effect is a broad movement toward greater security and prosperity for everyone, even the humblest. We have reached the point where even in the richest capitalist nation on earth, the system cannot provide minimal life security, or even basic life necessities for increasing proportions of the population. It was hard to escape the conclusion that the only way to restore us to lives of minimal decency was to come up with a different system entirely.

For my own part, the whole discussion might serve as a case study in the limits of statistical analysis. Not that such analysis isn’t revealing in its own way, but it all depends on what you set out to count in the first place. When I read through the tumblr page for the first time, what really struck me was the predominance of women’s voices, and the emphasis not just on acquiring the means for a decent life, but the means to be able to care for others. The latter was evident in two different aspects, actually. First was the fact that so many of those who chose to tell their stories worked in, or aspired to work in, a line of work that involved providing care for others: health care, education, community work, the provision of social services, and so on. Much of the terrible poignancy of so many of these accounts revolves around an unstated irony: that in America today, to seek a career that allows one to care for others usually means to end up in such straitened circumstances that one cannot properly care for one’s own family. This is, of course, the second aspect. Poverty and debt have a very different meaning for those who build their lives around relationships with others: it is much more likely to mean being unable to provide birthday presents for one’s daughter, or watching her develop symptoms of diabetes without being able to take her to a doctor, or watching one’s mother die without ever having been able to take her off for a week or two of vacation, not even once in her life.

There was a time when the paradigmatic politically self-conscious working-class American was a male breadwinner working in an auto factory or steel mill. Now it is more likely to be a single mother working as a teacher or a nurse. Compared to men, women are more likely to enter college, more likely to finish college, and more likely to be poor, the three elements that often lead to greater political consciousness. Labor union participation still lags slightly: only 45 percent of union members are women, but if current trends continue, a majority will be women in eight years. Labor economist John Schmitt observes: “We’ve seen a big increase over the last quarter century of women in unions, particularly as the unionization of the service sector expands”, he states. “The perception that unions are great for white guys in their 50s is false”.

Moreover, this convergence is beginning to change our very conceptions of work. Here I think Konczal got it wrong. It’s not that the 99 percenters are not thinking about the dignity of labor. Quite the contrary. They are broadening our conception of meaningful work to include everything we do that isn’t for ourselves.

Chat GPT: Yes, both Christianity and Islam traditionally forbid usury, though their interpretations and applications can differ significantly.

In Christianity, the prohibition of usury was more emphasized in the past, particularly during the Middle Ages. Usury, which was defined historically as charging any interest on loans, was condemned by the Catholic Church and other Christian authorities. This stance has evolved over time, and modern interpretations generally permit lending at interest, as long as the rates are not exploitative. Various passages in the Bible, especially in the Old Testament, such as Exodus 22:25, Deuteronomy 23:19-20, and Leviticus 25:35-37, advise against charging interest on loans made to the needy or one's community members.

Islam strictly prohibits all forms of usury, which it calls "riba." The prohibition is firmly rooted in the Quran and Hadith (sayings and actions of Prophet Muhammad). The Quran explicitly forbids riba in several verses (e.g., 2:275-279, 3:130, 30:39), making it clear that any gain or profit derived from loans of money, where the lender makes a return simply from the amount loaned, is considered an unjust and exploitative practice. Instead, Islamic finance relies on risk-sharing methods of investment and profit-and-loss sharing models, such as Murabaha (mark-up financing) and Musharaka (joint venture).

These religious teachings have led to the development of distinct financial practices and institutions, such as Islamic banking, which adheres to these principles.